........ reflecting a poor business investment outlook, weakness in commodity prices, the Australian dollar remaining too high and slowing momentum in home price growth.

As widely expected, the RBA left interest rates on hold at its August board meeting. While it appears to retain an easing bias with its assessment that growth is “below longer-term averages” and that the economy is likely to have “a degree of spare capacity for some time yet”, it appeared to soften this bias by removing its previous reference to a further fall in the Australian dollar seeming “both likely and necessary”.

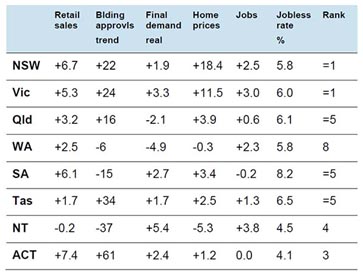

I am not in the gloomy camp on the Australian growth outlook. Low interest rates and the collapse in the value of the Australian dollar are helping the economy to rebalance which is seeing those sectors of the economy that were repressed through the mining boom return to strength. This is reflected in a reversal of the "two speed economy" which has seen Western Australia drop to the low end of a comparative ranking across the states and territories and Victoria and NSW push to the top.

Ranking the states, annual percentage change to latest

Source: ABS, CoreLogic RP Data, AMP Capital

However, it’s likely that the economy will still need more help. There are five main reasons why the RBA will likely move to cut interest rates again, probably before year end.

Reason 1 - The outlook for business investment remains poor

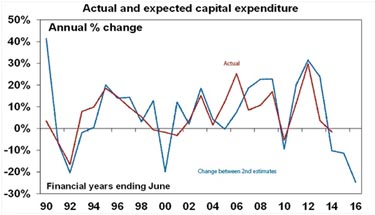

This was clear from the last ABS survey of investment intentions, released after the RBA last cut rates back in May. Comparing the latest estimate of investment for 2015-16 with that made a year ago for 2014-15 points to a 25 per cent fall in business investment in 2015-16 (see the next chart) and another approach points to a 23 per cent fall.

Source: ABS, AMP Capital

Resource investment is now falling rapidly back to 2 per cent of GDP as large projects complete. To offset this we need to see growth in other parts of the economy pick up and we have seen some success with housing and consumer spending. However, non-mining investment remains poor, with capex plans pointing to renewed weakness this financial year. There are several reasons why non-mining investment remains weak, including non-mining corporate scepticism after the battering they took through the mining boom (thanks to the strong Australian dollar, high interest rates and competition for labour), post-GFC caution and excessive project hurdle rates for a very low inflation world. High dividend payout ratios are not a factor because for industrial companies, payout ratios are within their normal range – they are up for the whole share market but this is due to resources companies and it is hard to expect them to invest more! At its core, the weakness in non-mining investment partly reflects the degree to which the natural rate of interest has fallen and the RBA has yet to fully reflect this.

Reason 2 – Commodity prices are weaker than anticipated

The continuing decline in commodity prices that is rolling though iron ore and coal, metals and energy prices, largely on the back of increased supply, is taking Australian export prices and the terms of trade far lower than has been anticipated by both the government and the RBA. Goods exports prices fell by another 4.4 per cent alone in the June quarter. This is resulting in a greater than expected drag on national income.

Reason 3 - The Australian dollar remains too high

It’s typical during a commodity slump for the Australian dollar to fall way below the fair value level suggested by purchasing power parity, which is currently around US$0.75. This is necessary to help sectors that were harmed through the prior mining boom by the high Australian dollar, including tourism, education, manufacturing and farming. This is now starting to happen, but at US$0.73, it's early days. While the US Fed is on track to raise rates later this year, still moderate US economic growth and weak wages growth and inflation pressures indicate it could be delayed and/or it could do just one move and wait a while. To ensure the Australian dollar continues on its downwards trajectory the RBA needs to keep jawboning it lower and likely cut rates again. In this regard it was disappointing and risky to see the RBA drop its reference to a further depreciation in the Australian dollar being “likely and necessary” in its August post-meeting statement.

Reason 4 - House price momentum is likely to slow in Sydney and Melbourne

Bank moves to tighten conditions for property investors via tougher income tests, lower loan-to-valuation ratios and higher mortgage rates in response to pressure from APRA are likely to weaken investor property demand and result in lower growth in home prices in Sydney and Melbourne. With property price growth comatose in the rest of Australia, at just 0.9 per cent on average over the 12 months to July, this will help reduce a major barrier to further RBA easing.

Source: RP Data, AMP Capital

Reason 5 - Monetary policy has recently been tightened

Bank interest rate hikes for both new and existing property investors amount to a de facto monetary tightening. While it’s only modest after tax it could become serious if banks respond to the increase in their funding costs as they move to put more capital aside for property lending as directed by APRA and raise interest rates for owner-occupiers. With economic growth still soft, higher mortgage rates across the board is certainly something that the RBA won’t want to see at this point in the cycle. The best way for the RBA to offset or neutralise this is to cut interest rates again.

Implications for investors

There are several implications for investors.

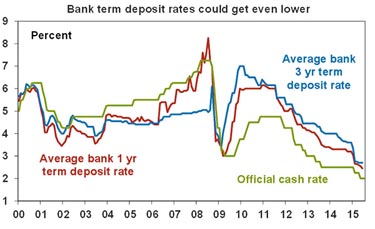

First, bank term deposit rates are likely to remain unattractive and could fall even further. We have to get used to ongoing low interest rates and investors still relying heavily on bank deposits need to consider what is most important to them: capital stability (in which case stick with bank deposits) or decent and more stable income flows (in which case various alternatives are arguably much more attractive).

Source: RP Data, AMP Capital

Second, ongoing low interest and deposit rates mean that growth assets providing decent yields will remain attractive. This includes commercial property and infrastructure but also Australian shares which continue to offer much higher income yields – and more stable income flows – than bank term deposits

Source: RBA, Bloomberg, AMP Capital

Finally, despite the 1 per cent post-August meeting bounce in the value of the Australian dollar, it is likely to remain in a declining trend as the interest differential in favour of Australia continues to narrow. So it makes sense to continue to have a greater exposure towards unhedged international assets than would have been the case say a decade ago when the trend in the Australian dollar was up.

Shane Oliver, head of investment strategy and economics and chief economist, AMP Capital

Columnist: Shane Oliver

Wednesday 5 August 2015

smsfadviseronline.com.au

28th-August-2015 |